by Troy Nix, executive director, MAPP

America’s insurance company giants receive billions and billions of dollars in profit, yet the cost of providing health insurance continues to challenge US manufacturers both large and small, and the impact of the pandemic has only added fuel and complete confusion to the fire.

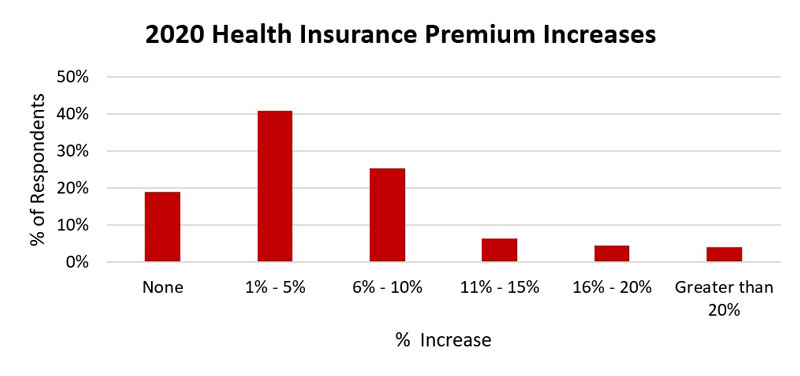

According to the most recent study conducted in 2021 by the Manufacturers Association for Plastics Processors, eight out of 10 executives reported that their health insurance rates increased in 2020, with 38% reporting a rise of from 6% to more than 30% (Chart 1).

More frightening, however, is the fact that nearly one in two executives in the polymer industry are experiencing or anticipate experiencing an increase of this same range. And, if one assumes size matters, assume again – large companies were just as prone to increases as smaller companies.

The recent survey conducted by MAPP, which combined forces with two other national manufacturing associations – the American Mold Builders Association (AMBA) and the Association for Rubber Products Manufacturers (ARPM) – collected data from more than 200 companies and covering nearly 27,000 employees in manufacturing. The 2021 Health and Benefits Report found that 99% of the surveyed population provides health insurance options to their employees.

According to an article published on Manufacturing.Net, the cause of rising costs is price, not utilization. Not only are there fewer physicians in the United States than in other industrialized countries, but there are fewer hospitals available and higher administrative costs. Also, the US has higher diagnostic costs and procedure costs – in fact, the US does more MRI and CT scans than any other country. Another contributing factor is the amount the US spends per capita on pharmaceuticals (this number is nearly double what other industrialized countries spend).

The most recent study conducted in 2020 by the Kaiser Family Foundation, a nonprofit organization focusing on national health issues, reported last year’s average annual premium for single health coverage was $7,470; the average annual family premium was $21,342. ARPM’s report revealed that the average annual premium per employee is $10,141.

To combat escalating changes in healthcare costs, executives are exploring a wide variety of options (Chart 2). However, 50% of the survey respondents have no real strategy for dealing with the variables affecting their most inflationary expenditures. In fact, the majority of the tactics being used today are ones that have been used and reused by employers for the last two decades and truly do not address long-term viability or the core issues that impact the ability to provide insurance benefits to employees.

Currently, the most popular tactic – used by 42% of surveyed executives – pertains to the use of Health Savings Accounts (HSA). The utilization of high-deductible health plans is a close second at 41%. Other notable tactics being implemented to offset rising costs include the use of flexible spending accounts (32%), Section 125 Plans (30%), wellness plans (27%) and dropping dependent coverage (5% of the surveyed population).

Unfortunately, nearly one in four executives are cost-shifting premiums to their employees. In other words, leaders are moving more of the expense of insurance to the employment base – an approach that is estimated to negatively impact employee retention as the battle for talent continues to be the number one challenge of the US-based business community.

Strategies addressing the core issue

This report does reveal that a small segment of organizational leaders are using true strategies to insulate themselves against health insurance premium escalation. A total of 9% of the population now is using captive funding arrangements to buffer themselves against market fluxuations. Although insurance captives have been in use for decades, it is very importrant to note that nearly every insurance captive operates differently. However, a basic princple of insurance captives is to control the insurance dollars and to either eliminate or reduce the opporunity for the insurance companies to make profits and recapture profits on the dollars spent.

The second strategy being used by approximately 6% of the population pertains to the use of onsite and nearsite clincs. This concept is contrary to most insurance business models and consists of providing free medical care and free commonly used generic medication to employees.

The reason the use of clinics is growing in popularity is that the model reduces the use of highly marked-up services and prescription drugs and makes it easier and more affordable for people to be proactive in their own personal care. Early detection and proactive care of health issues can be key to significnatly reducing long-term cost to address catostrophic issues.

The 2021 Health and Benefits Report covers a vast array of topics, including significant details on health insurance, the process of managing insurance, ancillary insurance benefits, prescription drugs, 401(k) plans and more.

More information: www.mappinc.com.