By Andrew Carlsgaard, business relations manager/analytics director, MAPP

According to feedback from 101 processing executives in MAPP’s 2023 Third Quarter Pulse Report, the near-term outlook for the US plastics industry going into the fourth quarter of 2023 is lukewarm; however, it is slightly higher than it was going into the third. The Pulse Report, conducted quarterly, aims to capture quarterly data points that will lead to insights that help executives better understand the current and projected near-term state of the plastics processing industry. Based on the report’s results from the first half of 2023, many processors started to feel the effects of a nationwide economic unease, though, with recession fears not manifesting as many prognosticators predicted, there is room for some optimism.

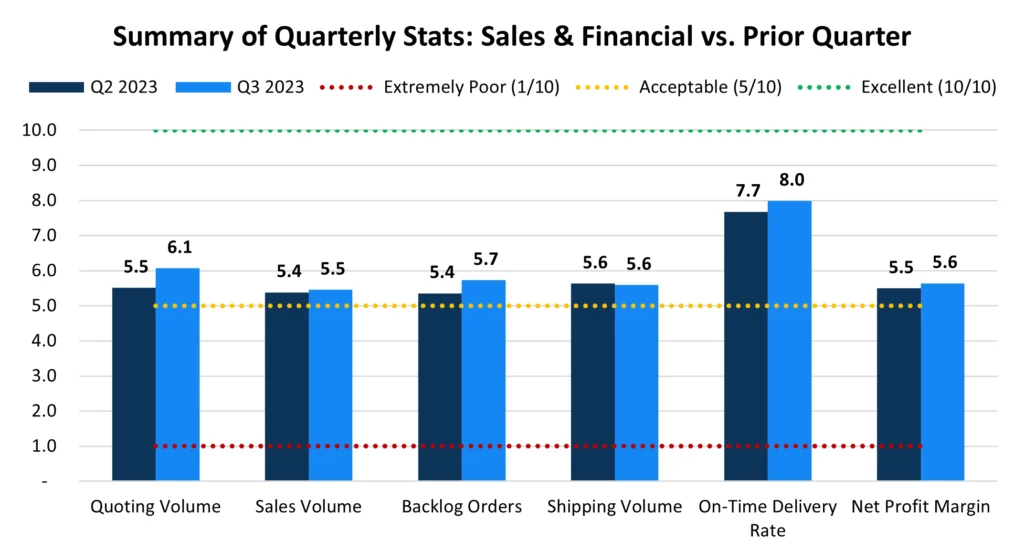

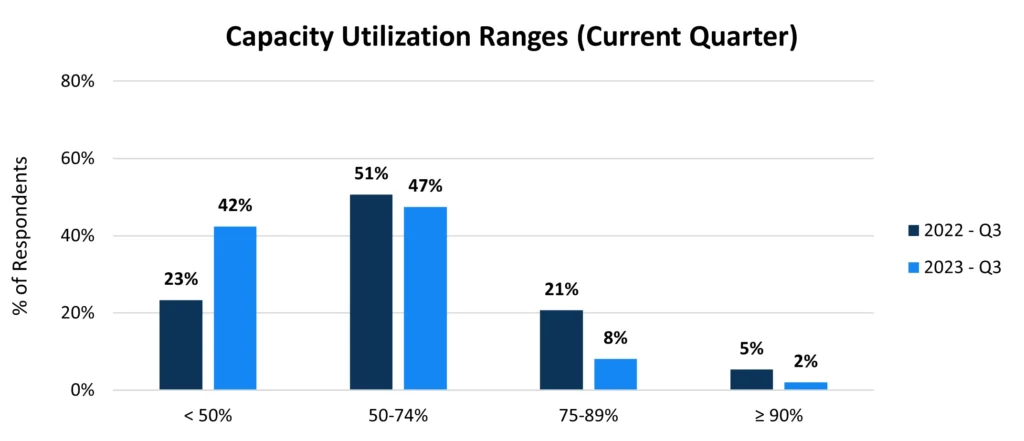

In a reversal of a recent trend, most of the quarterly sales and financial statistics in the Pulse Report increased on average compared to the prior quarter – those statistics were up on average by 0.2 points on a scale of 10. While this seems to be a positive takeaway, there are warning signs of future declines as third quarter capacity utilization (both current and expected for the next quarter) decreased approximately 9% (to 53% for both) compared to the same period a year ago. In addition, two out of five respondents (42%) reported having less than 50% capacity utilization – nearly a 20% increase from the previous year (23%). (See Charts 1 and 2)

Even though no official recession (defined as two successive quarters of GDP decline) has been called in the US, economic factors outside the plastics industry, such as the recent organized labor strikes at US automakers, make for a difficult and unpredictable environment for many processors. In the 2023 Third Quarter Pulse Report, about half of respondents (48%) reported that they do at least some levels of business with organizations that utilize organized labor, with 11% reporting doing “significant” amounts of business with those organizations. Nearly three-quarters (73%) of those processors in the “significant” category primarily serve the automotive sector. Respondents were asked to rate on a scale of 1-10 the potential negative impact current organized labor unrest will have on their business. The aforementioned half of respondents that do at least some level of business directly with unionized customers reported a level of concern of 3.9/10, while those 11% that reported a “significant” amount of business with such organizations reported a 5.6/10. As expected, those respondents doing business with unionized organizations primarily in the automotive sector experienced the highest level of concern (6/10) among all other primary market segments.

This elevated concern due to work stoppages at unionized customers could have negative effects on the economy broadly, especially considering other concurrent economic events in the US. As the Wall Street Journal’s1 David Harrison sums it up: “Among the possible challenges this fall: a broader auto workers strike, a lengthy government shutdown, the resumption of student loan payments and rising oil prices. Each on its own wouldn’t do too much harm. Together, they could be more damaging, particularly when the economy is already cooling due to high interest rates.”

Regarding the prospect of a prolonged strike, the WSJ reports that “A broader work stoppage could curb auto production and drive-up vehicle prices. Workers at auto-parts suppliers could also lose their jobs. A broad strike would shave off between 0.05 and 0.1 percentage point from annualized economic growth for every week it lasts, according to Goldman Sachs.” Experts cited in the article also expect growth to tail off significantly in the fourth quarter of 2023, compared to a relatively strong third quarter.

The road ahead in the fourth quarter of 2023 and forward into 2024 presents unique challenges. With heightened political and economic uncertainty going into an election year, plastics industry leaders must continue to adjust their business models to ensure continued profitability and future growth. Whether this means investing more in automation, diversifying the customer base or reexamining fixed expenses and headcount, this will require critical self-examination by decision-makers to find the appropriate solutions to fit their unique organizations.

The 2023 Third Quarter Pulse Report is available to purchase at www.mappinc.com.