By Andrew Carlsgaard, analytics director, MAPP

The fourth quarter of any year is a critical time for businesses. It’s a time when companies can either build on their successes, giving themselves momentum going into the new year or fall behind their competitors. MAPP’s 24th annual State of the Plastics Industry Report aims to explore the status of fourth-quarter momentum in the US plastics industry from 2023, and how it can be analyzed to forecast growth and success going into 2024. Slower-than-expected economic growth, inflation, labor shortages, wars and government interventions have made market conditions difficult to predict for the plastics sector in the post-COVID era. To best track these fluctuations and capture momentum for 2024, MAPP surveyed 185 plastics manufacturing companies across 34 states on the status of relevant industry indicators, ranging from quoting to resin supply to operator wages. The results of these benchmarks for 2023 performance (both for the entire year and fourth quarter specifically) indicate increased uncertainty and tempered optimism about 2024’s performance, despite improvements over the past year in some categories relative to a significant downturn in performance in 2022

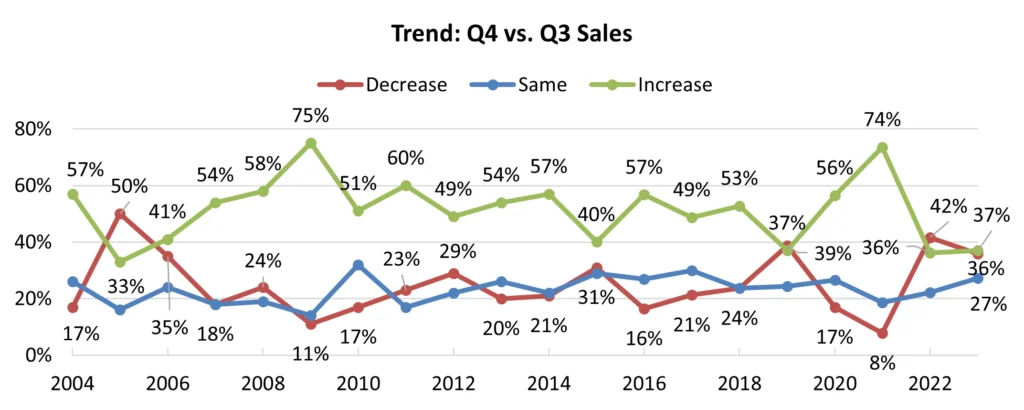

The focus on revenue growth and margin in the upcoming 2024 fiscal year likely will be strongly influenced by 2023 sales performance, particularly with substandard momentum when comparing quarter four to quarter three sales growth. Last year’s State of the Plastics Industry Report showed a considerable decline in sales performance in the fourth quarter of 2022, which led to 45% of respondents reporting a year-over-year sales decrease for the full year of 2023. For context, those processors indicating a sales decline over the same period at the end of 2022 was up to 42%, which marked the most

significant negative variance in sales performance in the 21-year history of publishing this statistic in the State of the Plastics Industry Report. Although the 2023 fourth-quarter sales performance showed that the negative momentum had eased slightly, 37% of plastics processors, nearly four out of 10 surveyed, still experienced a sales decrease from the prior quarter

(Chart 1).

To put things in a historical perspective and better understand how sales can drag industry momentum down going into a new year, examining the five-year trend average of processors indicating increasing sales performance transitioning from third to fourth quarters provides more reason for concern. On average, over the last five years, 51%, or half of the surveyed population, have reported gains from the third to fourth quarter; however, only 37% reported increases in Q4 2023. Additionally, of the sales increases organizations experienced in 2023, about a third (32%) were due to new customers. This trend has continued over the past two years, potentially signaling an expansion of the industry’s client base over the past three years. The share of new sales coming from increased volume in current programs from existing customers has declined from two-thirds (67%) in 2020 to 43% in 2023. However, momentum takes a slight positive shift when viewing sales over the next 12 months and asking processing executives to forecast top-line revenue over the next year. This year, 76% of respondents anticipate sales increasing over the next 2024 calendar period (Chart 2).

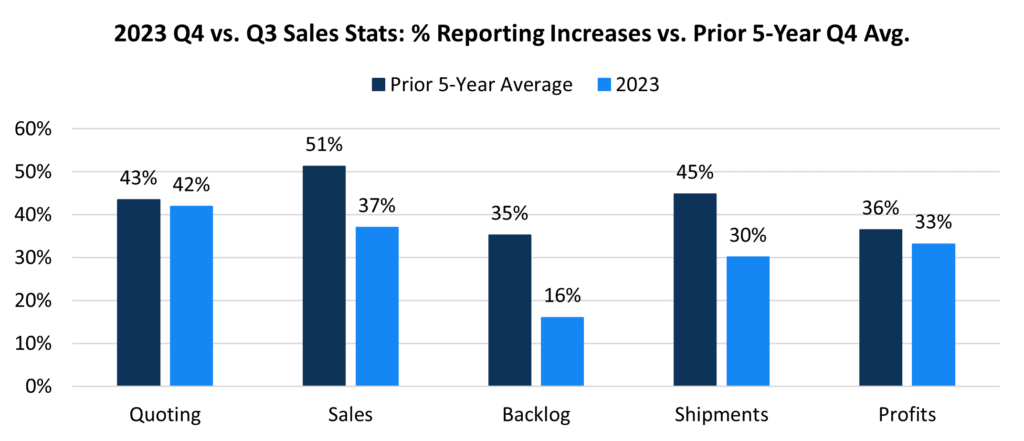

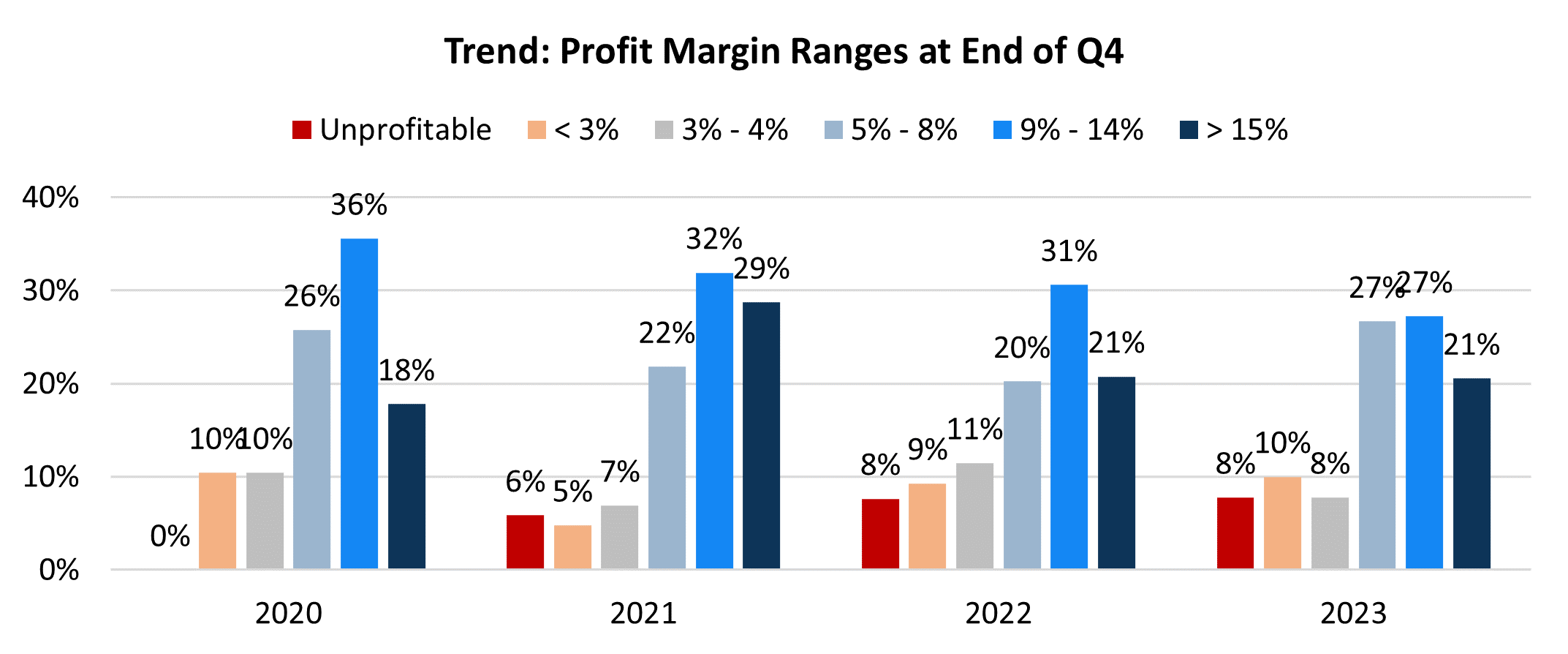

These uncharacteristically slower sales increases at the end of 2023 also resulted in lower overall profits, as only around a third (33%) of the surveyed processors indicated that their profit (net income) had increased since the end of the third quarter of 2023 – down from 50% for the same time in 2021, but an improvement from a mere 27% in the final quarter of 2022. To top things off, relative to forecasting a slower start to 2024, other business metrics outlining performance over the last two quarters of 2023, including fourth-quarter shipments, quoting trends and backlog, were all below the five-year trending averages. With these quarter-over-quarter performance figures in the books, processing executives must continue to navigate an environment with challenging obstacles to reaching their business goals. Of the reasons cited by respondents as their top three challenges interfering with profit margins, the most common were rising inflation, increasing employee wages and declining sales – the same top three as a year ago. While nearly three-quarters of the respondents (74%) still realized profit margins of 5% or more for the year in 2023, the bottom-line margin is down by nearly 800 basis points from the highs of 2021, while almost one out of 10 now sees their business as unprofitable for the second straight year

(Chart 3).

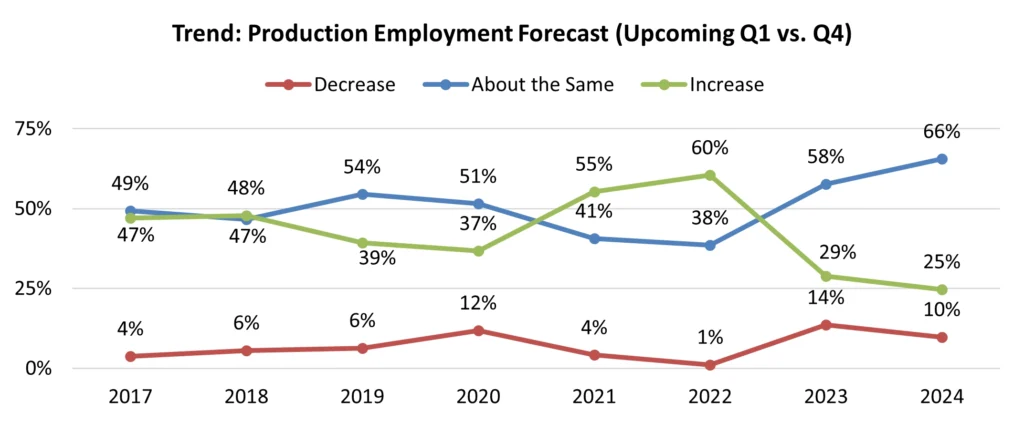

While this recent trend in decreased profits would appear to preclude cuts in major expense areas to offset, processors also felt that now is the time to invest in their businesses. Planned capital expenditures will increase in 2024 for over half of the participants – up from 42% for the 2023 forecast. The top categories for capital spending dollars over the next year were primary machines, automation and infrastructure, and respondents consistently cited these as critical pieces of their strategies to expand their businesses’ capabilities, upgrade their current automation builds and improve efficiency. However, as demand and capacity utilization remain low, employment levels in the first quarter of 2024 are expected to stay the same as the previous quarter for over two-thirds of respondents, while during the same period in 2022, nearly two-thirds of processors planned for staffing increases following a fruitful fourth quarter. Likewise, almost 80% of executives expect production employee work weeks in the first quarter of 2024 to stay level with the work weeks preceding it.

Despite the challenges processors faced over the past couple of years during a turbulent time in the US economy, leaders have found ways to successfully fend off significant industry-wide challenges. The lessons learned and adaptations made will hopefully lead to a more porfitable 2024. Despite year-end momentum being down compared to some recent highs, the industry’s status compared to this same point last year is positive, with optimism that processors likely will exceed expectations in 2024. With its members’ help and input, MAPP will continue to strive to equip its members with the best intelligence available in the industry and allow them to thrive in today’s dynamic global economy.

Further analysis is available by purchasing the 2024 State of the Plastics Industry Report through www.mappinc.com. The 2023 Machine Rate Report, with updated machine rates as of December 2023, now is available for purchase at www.mappinc.com. If interested in becoming a member of MAPP, email info@mappinc.com.