By Andrew Carlsgaard, business relations manager/analytics director, MAPP

The changing dynamics between employers and the US workforce over the last few years have affected wages and salaries for nearly every job in the manufacturing industry. While wages and salaries in the US plastics manufacturing industry can vary depending on several factors, including job role, skill level, experience and geographical location, the recent trend has skewed toward higher wages for workers amid increased demand for products and services post-2020. These observed increases partly are due to near double-digit inflation and a decreased supply of workers.

According to the US Bureau of Labor Statistics, workforce participation hasn’t rebounded from pre-pandemic levels as of May 2023, and still is 2.5 million workers short when compared to February 2020. Unemployment spiked to over 14% at the height of the pandemic but has been comparable to pre-pandemic levels since early 2022. A reported 0.56 ratio of unemployed persons per open position as of April 2023, is at a record low and has been maintained since late 2021. Low unemployment, plentiful job openings and relatively low participation have made somewhat of a buyer’s market for workers in the past few years, who constantly feel the pressure to find higher wages to offset inflation. However, inflation is slowing in the current year, and potential economic headwinds could see that trend slowing in 2023.

The 2023 MAPP Wage and Salary Report provides valuable insight into salaries across the plastics industry. The industry offers a range of employment opportunities across numerous sectors, including medical, consumer goods, industrial plastics product manufacturing and plastics product wholesale and distribution. Additionally, individuals with specialized knowledge in areas like polymer science, materials engineering, automation or plastics technology may earn higher wages than others at similar levels due to the demand for their expertise. Geographical location also impacts wages within the industry, as certain regions with a strong concentration of manufacturing facilities (and competition for workers) or a higher cost of living may offer higher wages to attract and retain skilled employees.

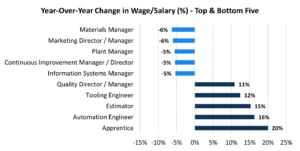

In the 2023 report, 54 of the 67 historically tracked positions (81%) increased median compensation (up from 76% in the previous year). The average increase year-over-year for those positions was approximately 6%. The remaining 13 positions decreased in median salary – averaging around 3% lower than in 2022. Overall, tracked salaries increased by 4% from 2022. The most substantial salary increases between 2022 and 2023 were for apprentices (20%), automation engineers (16%), estimators (15%) and tooling engineers (12%). Conversely, the most substantial median wage decreases were for materials managers (-6%), marketing managers and directors (-6%), plant managers (-5%) and continuous improvement managers and directors (-5%) (see chart 1).

A new trend for 2023 was that white-collar workers and managers less involved in the plant’s day-to-day operations most often saw declines year-over-year compared to those closer to operations or engineering. Moreover, having a high-demand specialty gives certain segments of employees (such as automation engineers) more sway in negotiating rates.

While the average yearly wage increase seems relatively high, inflation likely accounts for much of this. The consumer price index (tracked by the Bureau of Labor Statistics) peaked a year ago, in June 2022, at around 9.1%, but this has been falling since then and sits at 4.1% as of May 2023, remaining twice as high compared to pre-pandemic levels). Inflation, on average, sits at 5.3% for 2023 (see chart 2). Comparing that 4.1% May inflation figure to the approximately 4% growth on average for all positions tracked in the 2023 Wage and Salary Report (data captured from May and June 2023), it’s clear that inflation is the primary driving factor for the general increase in the past year. Also, despite these year-over-year increases, processors report slightly lower hiring demand overall than last year.

In 2022, 92% of those surveyed said they would be hiring new employees over the next 12 months, and this dropped to 87% in 2023. While this only is a 5% decrease compared to the previous year, there may be some concern that a recession likely is around the corner due to recent government intervention to curb consumer demand and inflation. Hiring new roles more slowly than in the previous few years or maintaining a consistent level of employment may prevent any future reduction in workforce. When the recession hits and unemployment increases, employers likely can expect to see the trend in rising wages tail off or potentially decrease as demand for new employees decreases and hiring slows.

The salary and wage increases observed in the 2023 report are not surprising, given the current state of the economy and inflationary pressures. Depending on the situation, processors may need to adjust to remain competitive in the labor market or risk losing valuable resources and incurring additional costs to replace departed employees. If conditions remain favorable toward workers, there will continue to be some degree of movement in the market.

Knowing the going rate for those positions is imperative to attracting and retaining the necessary talent to keep operations steady in an uncertain economy. Likewise, if the market shifts toward employers in a recession, processors only need to adjust to the current market if it fits the current needs of their business. The 2023 MAPP Wage and Salary Report contains a detailed breakdown of all 67 industry positions, an analysis of benefits and data on additional forms of compensation to help prepare regardless of market conditions.

Discover the latest wage and compensation rates, along with the most recent workforce management benchmarks covering shift differentials, overtime, PTO and more:

www.mappinc.com