by Ian Gjertson, analytics director, MAPP

The past two years featured numerous challenges and controversy as the world has tried (and continues to try) to adapt to and overcome the COVID-19 pandemic. Fortunately, according to the 195 plastics processing companies that participated in MAPP’s 22nd annual State of the Plastics Industry Report, which benchmarks 2021 performance metrics and 2022 expectations, there are several auspicious reasons to be optimistic about the upcoming year.

Last year’s State of the Plastics Industry Report forecasted 2021 as a comeback year for plastics processors, and these expectations did not disappoint. Despite navigating the chaotic supply chain network, challenging labor recruitment and retention, escalating inflation, intensifying resin prices and lead times and increasing wage expectations, most plastics processors consistently experienced an increase in quoting and sales volume throughout 2021.

77% of the surveyed companies achieved an average annual sales increase of 18% by the end of 2021, making it the highest average annual sales increase MAPP has recorded in the past five years. Additionally, half of the processors indicated that their profit (net income) had increased since the end of the third business quarter (September 2021), with 27% that experienced no change and 23% that experienced a decrease in profit.

Nearly every fourth-quarter performance metric in this year’s report is higher than it has been in 18 years. The most substantial differences are backlog orders, inventory, production employees and sales volume. Despite managing constant external disruptions in 2021, such as the surging United States inflation rate, these upward performance trends illustrate that processors successfully implemented effective strategies and tactics.

More than half of surveyed processors listed the rising resin prices as one of their top three challenges. The average resin price increased by approximately 8.5% between the third and fourth business quarters. Due to the rising resin price, 89% of surveyed processors passed on 81% of their total resin price increases to their customers. Additionally, a little more than one-fifth of processors identified resin lead times and almost one-third of processors identified the supply chain network as one of their top three challenges. Since last July, more than 80% of processors indicated that resin lead times continuously have worsened. Processors need to implement inventory optimization strategies and increase visibility with resin suppliers as the chaotic global supply chain network issues continue into 2022.

70% of processors purchase production tooling from offshore suppliers. The most common countries of origin for production tooling include the United States, China, Canada, Taiwan and Germany. More processors are experiencing higher prices and longer lead times for domestic-based tooling vendors when compared to foreign-based tooling vendors.

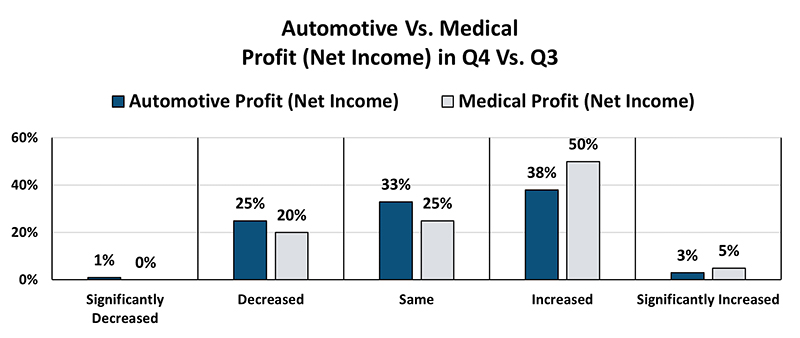

These challenges have not had an equal impact on every market segment. Processors have identified the medical market segment as the most optimistic segment for the fourth consecutive year. Meanwhile, more than one-third of surveyed processors perceive the automotive market segment as the most pessimistic market segment for 2022. These forecasts likely are due to the difference in performance between the two market segments in 2021. More than half of the processors that serve the medical market segment experienced increased profit levels, while only one-fifth experienced a decrease in profit. Nearly 60% of processors that supply the automotive market sector experienced no change or decreased profit levels in the fourth quarter of 2021.

These challenges have not had an equal impact on every market segment. Processors have identified the medical market segment as the most optimistic segment for the fourth consecutive year. Meanwhile, more than one-third of surveyed processors perceive the automotive market segment as the most pessimistic market segment for 2022. These forecasts likely are due to the difference in performance between the two market segments in 2021. More than half of the processors that serve the medical market segment experienced increased profit levels, while only one-fifth experienced a decrease in profit. Nearly 60% of processors that supply the automotive market sector experienced no change or decreased profit levels in the fourth quarter of 2021.

On average, processors anticipate that sales will increase in 2022 by approximately 12% compared to 2021, which is the highest sales increase forecasted in the annual State of the Plastics Industry Report for the past five years. Companies that generate less than $5 million in annual revenue anticipate the highest increase at 19% sales growth, while companies that yearly generate between $15 and $50 million in revenue anticipate the lowest sales growth at 9%.

70% of surveyed processors anticipate their capital expenditure will increase or significantly increase in the next 12 months. Almost four of every 10 plastics processors intend to implement automation as a competitive advantage in 2022, most likely due to the increasing and universal difficulties in recruiting, retaining and compensating employees. In 2022, processors will invest 46% of total capital expenditure in primary machinery and 30% in automation technology.

Although obstructions such as the supply chain network issues, material shortages, international tensions and potential government interference likely will continue in 2022, processors can be optimistic about the increasing demand for plastic components.

Further analysis is available by purchasing the 2022 State of the Plastics Industry Report through www.mappinc.com. If you are interested in becoming a member of MAPP, please email the MAPP staff at info@mappinc.com.