by the Manufacturers Association for Plastics Processors

The Manufacturers Association for Plastics Processors (MAPP), in response to processing executives’ request for data to better understand the impact of the COVID-19 pandemic, began generating biweekly “pulse” reports in the early part of April 2020. These pulse reports cover a wide range of business information, including plant operating levels, supply chain disruptions, customer shutdowns, current and future staffing level expectations, revenue performance and more.

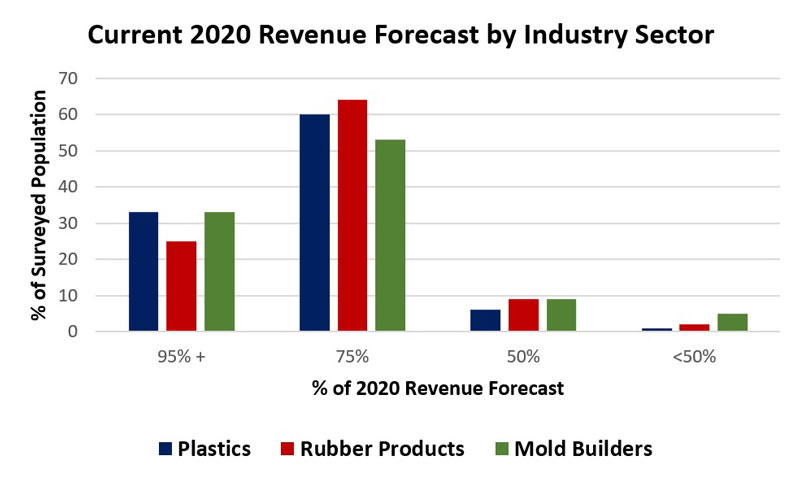

“It’s obvious that the COVID-19 pandemic has crushed the US economy, and if one wants to better understand how the crisis has directly impacted the plastics manufacturing community, the damage can be found in the updated sales revenue forecast trend,” stated Troy Nix, MAPP executive director, in a recent interview. “It’s alarming to know that if 100 plastics manufacturing companies were polled today, 60 companies would be performing to 75% of their 2020 revenue plans, six organizations would at 50% of their annual forecast and one entity would be tracking below 50% of the annual plan. That means that only one third of the industry is operating as if this were a normal year!”

Product or industry mix has a great deal to do with where plastics processing businesses are performing on their actual-to-plan revenue for 2020. Of the more than 200 company professionals completing MAPP’s most recent pulse survey, those primarily serving the medical marketplace were the most likely to have the most favorable outlook on revenue for this year. 51% of the medical processors are running at 95% or higher of their 2020 forecast; 47% are tracking at 75% of their forecast. However, it is important to understand that revenue projections from those processing executives serving the medical marketplace have been slowly degrading over the past several weeks. As an example, at the beginning of June, 66% of the manufacturing community primarily focused in medical products were tracking to their 2020 budgeted revenue; by the middle of June, only 51% were on track, representing a 15-point reduction.

Plastics manufacturing businesses primarily serving the automotive sector have been hit the hardest, as only 7% of company executives responding to the latest survey are tracking to their 2020 budgeted revenue. Nearly three-fourths of companies serving automotive are forecasting revenue through the end of 2020 at 75% of their original 2020 forecast, while a staggering 19% anticipate revenue through the end of 2020 to be at 50% or below what they forecasted for the year.

It is to be noted that automotive suppliers’ customers remained shut down at higher levels and for longer periods as compared to any other industrial markets. As of the middle of June, nearly one quarter of the automotive suppliers completing MAPP’s pulse survey indicated that they were operating at the 25% to 50% level. To make matters worse, a total of 45% of leaders in the automotive sector anticipate minor to moderate supply chain disruptions over the next several months, which will continue to hamper operation efficiencies.

When plastics processing executives look over the proverbial fence to see if the “grass is greener on the other side,” they will find that they are faring far better than both the rubber products manufacturing sector and the mold building segment. These industries are projecting even worse revenue performance for this year, as can be viewed in Chart 1.

As identified in MAPP’s 2020 State of the Plastics Industry Report, completed in January of this year, one of the major challenges of the US processing sector was the attraction and retention of the workforce. At the time of this article, companies were asked to report on both their near and future term staffing plans and how those plans might change over the next six to 12 months. One brighter spot in current industry conditions is that the large majority, or 86% of the more than 200 companies that replied, indicated that their workforce development strategies entailed maintaining current employment levels and hiring additional employees in the near future. A small fraction, or 14%, indicated they will have some permanent or semi-permanent staff reductions over the next year.

As with the adjusted 2020 sales revenue forecasts, customer segment had an impact on the workforce development outlook of the executives responding to the survey.

Medical: 94% of companies primarily serving the medical industry indicated they will either maintain staff (49%) or add additional staff in the next six to 12 months (45%).

Automotive: More than any other industry, automotive was the most likely to be focused on maintaining staff levels or having some minor staff reductions. Nearly half (49%), are looking to maintain staff, and 16% are hoping to add staff in the next six to 12 months. However, the remaining 35% are reporting permanent or semi-permanent staff reductions for the near future.

Consumer Goods: 92% of executives supplying to the consumer goods marketplace reported a workforce development outlook similar to that of medically focused suppliers, as they are either looking to add staff (52%) or maintain staffing levels (40%) over the next six to 12 months.

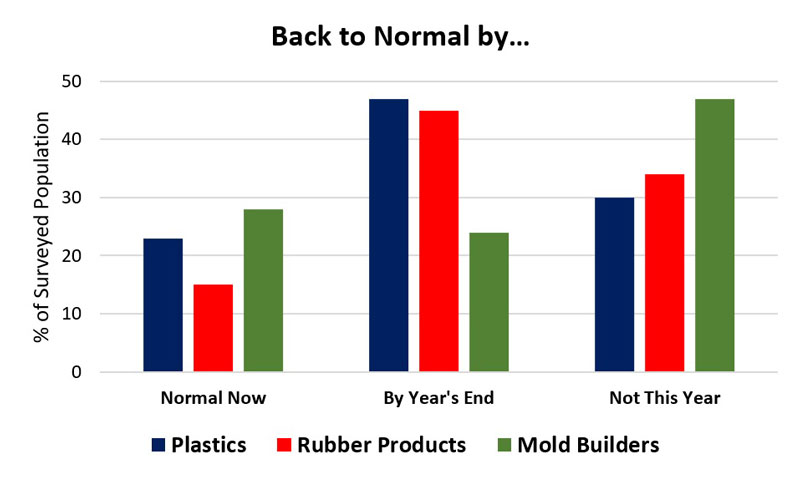

One question looming for all manufacturing executives: When will the crisis be in the rearview mirror? This is followed closely by, “When will things return to normal?” A good sign for the US economy is that the Purchasing Manager’s Index (PMI), a quantitative measure of the prevailing direction of economic trends in manufacturing, jumped to 52.6 in June. This was a 9.5 point increase from the month of May, which greatly surpassed market expectations.

Although the PMI has recorded an expansion number for the first time in many months, leaders in the plastics, rubber products and US mold building sectors have differing viewpoints about when business operations will return fully to normal. As many industry experts predicted delayed impact of the COVID-19 crisis on the US mold building industry, it appears as if the executives in the tooling building arena now agree: An astounding 47% have identified that they do not feel normalcy will occur in 2020. With stark contrast, business leaders representing both the plastics and rubber products sectors feel more optimistic about things returning to normal: 70% of plastics processors and 60% of rubber products leaders have either returned to normal or expect to be operating normally by year’s end.

To obtain the latest pulse survey results or other benchmarking information: www.mappinc.com