By Andrew Carlsgaard, benchmarking and analytics director, MAPP

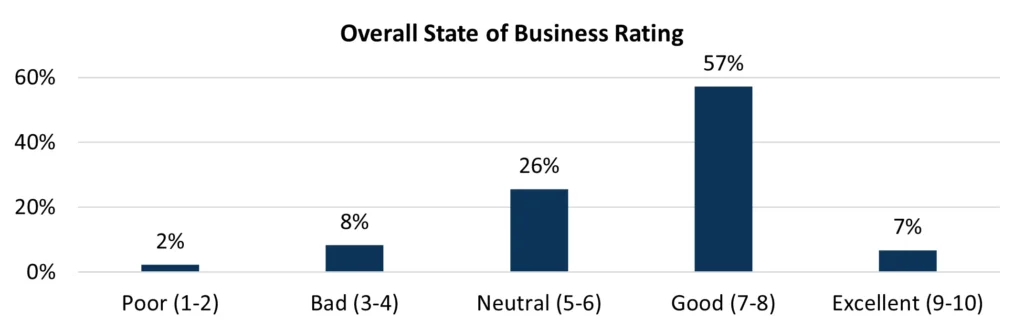

MAPP’s 26th annual State of the Plastics Industry Report, based on responses from 152 plastics processing leaders, depicts an industry that is stable and optimistic but also under increased profit pressure, with most companies operating in the middle of the performance spectrum rather than at extremes. Notably, over half of respondent processors place their overall state of business at the beginning of 2026 in the mid-range “good” category, while another quarter reports a “neutral” status. The overall average for this rating was 6.7/10. This above-average rating indicates that the sector has moved past the highly volatile conditions of the early 2020s. However, it has not returned to the more predictable growth of the previous decade. (Chart 1)

Fourth Quarter Reflections

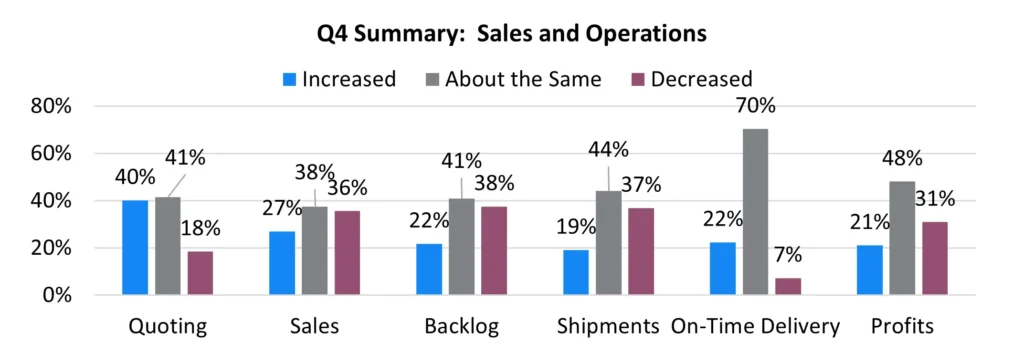

The survey aims to explore the business status of the US plastics industry in th han the severe contractions observed in previous years’ reports. However, most respondents report middling or negative fourth quarters, with sales volume, backlog, shipments and profits most often rated “about the same” or “decreased” compared to the prior quarter. (Chart 2)

Profit Margins Tighten as Sales Slow

Regarding sales performance, the slower sales increases at the end of 2025 also likely contributed to lower overall profits, as only around a fifth (21%) of the surveyed processors indicated that their profit margins (net income) had increased since the end of the third quarter of 2025, down from 33% for the same time in 2023. When examining margins for the full year 2025, nearly three-quarters of respondents (65%) still reported profit margins of 5% or more (down from 74% in 2024), while 11% reported unprofitable (up from 6% in 2024). Respondents reported a small average year-over-year increase in 2025 (3% on average) but a shift toward low-double-digit growth expectations for the next 12 months (13% on average), indicating that leaders view 2025 as a reset year and 2026 as a potential inflection point.

Additionally, capacity utilization at the end of 2025 averaged roughly half of total available capacity (52%), and typical respondents expect only a modest uptick at the start of 2026 (56%), reinforcing the picture of cautious deployment of existing assets rather than aggressive expansion to meet sales and margin forecast goals.

Ongoing Cost Pressures

Nearly a quarter of processors (21%) experienced resin cost increases in Q4 2025, and most report passing only around 51% of those increases through to customers (down from 76% in 2023), contributing to ongoing margin compression.

Workforce measures such as production headcount, workweek length and time to hire appear relatively steady in the data, though processor comments consistently point to recruiting, retention and wage and healthcare cost pressures as structural issues that erode margins even in otherwise stable markets.

Despite this, a clear majority (83%) of respondents say resin availability has “no impact” or only a “slight impact” on their operations in the fourth quarter of 2025, a sharp contrast with the more severe shortages seen earlier in the decade.

2026 Outlook with Optimism

When respondents are asked directly about their 2026 outlook, a higher share describes themselves as optimistic or somewhat optimistic about their own company’s performance (rated 6.4/10 on average) than about the plastics industry as a whole over the next 12 months (6/10), even though both measures reflect moderate optimism rather than exuberance. Many executives pair 2026 sales growth forecasts with specific strategic moves to protect or expand margins, highlighting initiatives such as investing in automation, new or upgraded software/ERP and employee development as their top planned activities to improve competitiveness.

Notably, over half of respondent processors place their overall state of business at the beginning of 2026 in the mid-range “good” category, while another quarter reports a “neutral” status.

Capital spending intentions align with this story: A meaningful share of respondents (73%) indicate that 2026 capital outlays will hold at or slightly above 2025 levels, and they most frequently earmark spending for automation, primary machines and repairs rather than large structural expansions. At the same time, the top-margin challenges – declining sales, rising inflation, uncertain government policies, employee wages and escalating healthcare costs – underscore that even modest growth will not automatically translate into stronger profitability without structural cost and capability improvements.

Looking ahead, respondents’ cautiously positive expectations for 2026 line up with the broader economic consensus for the United States, which anticipates slower but still positive GDP growth, fading yet persistent inflation, and a gradual easing of interest rates rather than a dramatic policy shift. Despite this, most processors still plan for modest sales increases (13.1% on average – up from 10.5% in 2025), though the prevalence of “no change” or “slight increase” responses for both capacity utilization and capital spending reflects a pragmatic growth posture. Within that posture, medical-heavy (40% or more of annual revenue) and stronger automotive-heavy firms tend to report higher planned first-quarter 2026 utilization and somewhat stronger growth expectations than industrial- and consumer goods-heavy peers, reinforcing the view that healthcare and automotive may be the more reliable demand engines in 2026.

Overall, the 2026 State of the Plastics Industry Report portrays an industry that has largely worked through its most acute supplychain and pricing disruptions over the past half-decade, and now is pivoting toward an efficiency- and technology-led growth model. Success in 2026 likely is to favor processors that can combine disciplined cost management with targeted investment in automation, people and highvalue market segments in an environment of modest macroeconomic expansion.

Further analysis is available by purchasing the 2026 State of the Plastics Industry Report through www.mappinc.com. If interested in becoming a member of MAPP, please email the MAPP staff at info@mappinc.com.