By Troy Nix, executive director, MAPP

Health benefits remain one of the largest – and most unpredictable – line items in a manufacturing company’s budget. Recent reporting underscores just how acute the challenge has become. According to The New York Post, US employers are facing projected healthcare cost increases of 7% to 10% over the next 12 months, the steepest rise in more than a decade. These increases are being driven by higher hospital costs, increased utilization and the rapid adoption of expensive therapies, including GLP-1 drugs.

For manufacturers operating on tight margins, this volatility creates real planning challenges. Yet for many employers using traditional fully insured, level-funded or conventional self-insured models, the annual renewal process feels increasingly one-sided. Premiums go up, plan designs tighten and explanations for those increases often lack clarity or actionable insight. Small- and mid-sized manufacturers, in particular, are left with little leverage and limited visibility into what actually is driving their costs.

It’s no surprise that many executives feel trapped in a perpetual “rate race.”

But it doesn’t have to be this way.

A Proven Solution

An increasing number of manufacturers are finding relief – and control – through healthcare captives, particularly those owned and governed by industry associations. While not all captive platforms are created equal, association-owned captives offer distinct advantages rooted in ownership, collaboration and aligned incentives.

At their core, captives are designed to fund health benefits in a more disciplined and transparent way. When structured properly, they allow employers to dilute risk, manage volatility and retain value that would otherwise be absorbed by commercial carriers.

The difference is simple but powerful:

- In traditional fully insured arrangements, carriers assume the risk and retain underwriting gains when claims run better than expected.

- In an association-owned captive, participating employers collectively dilute risk – and any surplus generated by good plan performance remains within the membership.

When claims are favorable and reserves are satisfied, value stays with the employers that funded the plan. When claims are adverse, predefined risk protections limit downside exposure. Over time, this model rewards prudent plan management rather than exporting profits outside the group.

Why Association Ownership Matters

The term “captive” can sound complex, but the objective is straightforward: align incentives, improve predictability and promote long-term sustainability.

Association-owned captives add a critical layer of governance. Because the platform is owned by its members and operated within the association’s framework, the goal is not to maximize profits for a third party. The goals are to:

- Manage risk responsibly.

- Operate with transparency.

- Deliver value back to participating employers.

This governance structure shifts health benefits away

from a transactional, year-to-year exercise and toward a long-term strategy – one that reflects the realities of manufacturing businesses.

CAPTIV8: A Competitive Advantage for MAPP Members

For members of the Manufacturers Association for Plastics Processors (MAPP), this advantage isn’t theoretical. It already exists – and it’s thriving.

CAPTIV8, MAPP’s association-owned healthcare captive, was built specifically for the plastics manufacturing community. Over the past five years, CAPTIV8 has delivered meaningful results for participating members, including:

1.Shared Savings That Stay with Members When CAPTIV8 performs well, underwriting gains are not automatically retained by an external carrier. After claims, expenses and required reserves are satisfied, surplus funds can be returned to participating members – effectively using yesterday’s dollars to help fund today’s claims.

2.Transparency into What Drives Costs CAPTIV8 participants receive deeper analytics and clearer insight into claims trends, large-claim drivers and utilization patterns. This level of transparency allows executives to make informed, targeted decisions rather than guessing at the cause of annual increases.

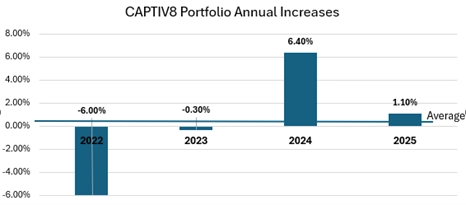

3.More Predictable Budgeting Through Smarter Risk Financing By pooling risk with peer manufacturers and utilizing structured stop-loss protection, CAPTIV8 reduces exposure to extreme claim volatility while preserving upside when claims outperform projections. Over the past three years, documented rate increases across the CAPTIV8 portfolio have averaged just 0.3% (Figure 1).

4.Collective Buying Power and Industry Expertise Few individual employers have the time or leverage to evaluate every vendor and strategy. CAPTIV8 enables collaboration within a trusted peer community while providing access to a team of nationally recognized experts focused on pharmacy management, plan design and cost-containment strategies tailored to manufacturers.

5.Incentives Aligned to Better Outcomes When members share in the upside, investments in preventive care, condition management and thoughtful plan design become strategic decisions – not sunk costs. The result is a virtuous cycle: healthier populations, fewer high-cost surprises and stronger long-term financial performance.

Changing the Conversation

Most employers ask the same question every renewal cycle: “How much more will we pay next year?” CAPTIV8 allows MAPP members to ask a better one: “How do we manage our plan well enough to share in the upside?”

The Bottom Line

CAPTIV8 is not simply an alternative funding mechanism. It is a member-owned strategy designed to keep value with the employers that create it. For MAPP members, the benefits are clear:

- Improved transparency

- Better risk management

- Collective buying power

- A model where favorable financial performance can be returned to the membership rather than being absorbed by outside carriers

In a world where healthcare costs often feel uncontrollable, CAPTIV8 offers a refreshing premise: When manufacturers collaborate with peers, govern responsibly and manage their plans well, they don’t just reduce uncertainty – they share in the results and get out of the rate race.

More information: contact MAPP at info@mappinc.com or send correspondence to Tony Robinson at trobinson@mappinc.com.