By Andrew Carlsgaard, business relations manager/analytics director, MAPP

Over the past year, there has been a significant fluctuation in the global economy in the prices of goods, services, and labor across all sectors due to the lingering effects of the Covid-19 pandemic. In addition, supply chain issues, labor shortages, oil prices, war and government intervention only have exacerbated these issues over the past three years. With double-digit inflation and recession fears on the rise, plastics processors’ expectations for a profitable new year in 2023 are lower than in years past.

To track these fluctuations, MAPP’s 23rd annual State of the Plastics Industry Report surveyed over 200 plastics manufacturing companies located in 32 States across the US over a wide range of topics, from quoting to resin supply to operator wages. The results of these benchmarks for 2022 performance and 2023 expectations indicate increased uncertainty and decreased optimism about the upcoming year, despite improvements over the past year in some categories.

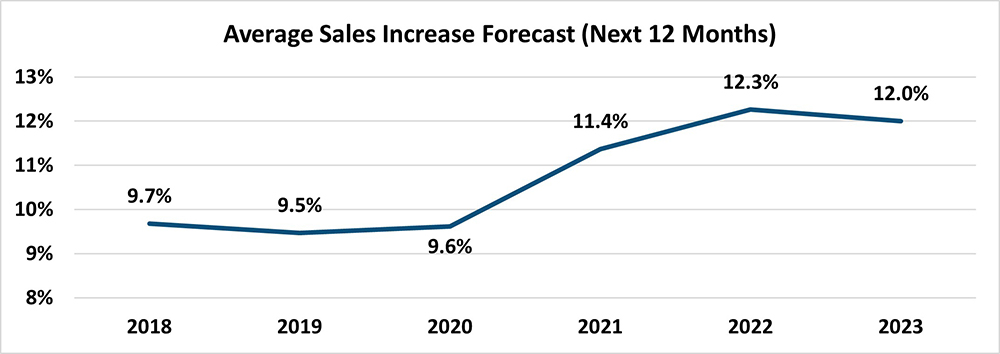

Last year’s State of the Plastics Industry Report forecasted 2022 to continue the solid rebound year for plastics processors in 2021. While sales increases beat expectations, they noticeably were less than respondents enjoyed in the previous year. Coming into 2021, processors surveyed were expecting a forecasted average sales increase of 11.4% but realized an increase of 18.3% (6.9% over expected), while in 2022, they saw 14.0% on a forecast of 12.3% (1.7% over expected). For 2023, expectations practically are level with 2022’s forecast at 12.0%. However, based on recent results, it would not be surprising if the actual increase returns to pre-2020 levels, as only 36% of respondents saw sales increases from the third quarter to the fourth quarter of 2022 (down from 74% Q3 to Q4 2021). This is the largest point drop in the past 19 years of the Survey for those indicating an increase in sales from Q3 to Q4, compared to the previous year at nearly a 38-point difference. On the flip side, those processors indicating a sales decrease over the same period at the end of 2022 was up to 41%, which ties the results from 2005 for the largest percentage increase from the prior year at 33%.

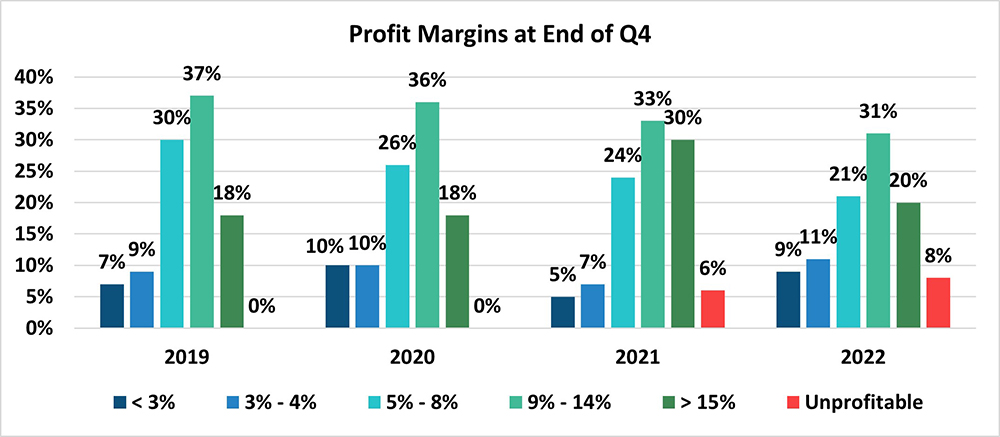

These uncharacteristically slower sales increases at the end of 2022 also resulted in lower overall profits, as only around a quarter (27%) of the surveyed processors indicated that their profit (net income) had increased since the end of the third quarter of 2022 – down from 50% for the same time in 2021. Despite processors experiencing an overall increase in quoting and sales volume in 2022 and an improved supply chain for resin, they expect to continue to navigate an environment with challenging labor recruitment and retention, increasing wage expectations and inflated tooling and resin prices that will cut into the bottom line. Of the reasons cited by respondents for “top 3 challenges interfering with profit margins,” the most common were rising inflation, increasing employee wages and declining sales. While most respondents (72%) still realized profit margins of 5% or greater, these are down from 2021 by 15%, and 8% now see their business as unprofitable.

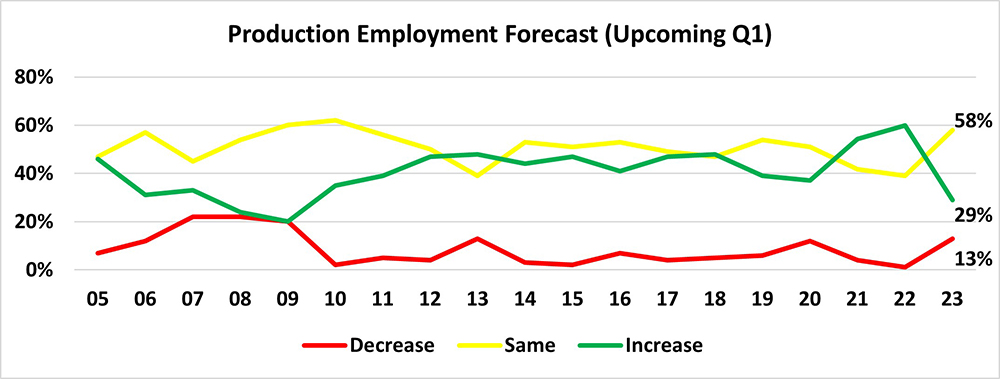

This recent trend in decreased profits could see cuts in major expense areas to offset, as nearly two-thirds of respondents expect capital expenditures to decrease or stay the same in 2023 – up from one-third for the 2022 forecast. Additionally, with lower-than-expected sales and decreasing backlog, production employment to start the new year is expected to decrease or stay the same in 2023 for nearly three-quarters of respondents, while in 2022, nearly two-thirds of processors planned for staffing increases.

This recent trend in decreased profits could see cuts in major expense areas to offset, as nearly two-thirds of respondents expect capital expenditures to decrease or stay the same in 2023 – up from one-third for the 2022 forecast. Additionally, with lower-than-expected sales and decreasing backlog, production employment to start the new year is expected to decrease or stay the same in 2023 for nearly three-quarters of respondents, while in 2022, nearly two-thirds of processors planned for staffing increases.

While processors have continued to weather the storm successfully this past year and have fended off significant challenges to the plastics processing industry over the past three years, the road ahead will likely require increased fortitude and adaptability to exceed expectations and come through 2023 even more resilient. With the help and input of its members, MAPP continues to strive to provide meaningful insights to equip its members with the best intelligence available in the industry to grow and thrive in today’s dynamic global economy.

While processors have continued to weather the storm successfully this past year and have fended off significant challenges to the plastics processing industry over the past three years, the road ahead will likely require increased fortitude and adaptability to exceed expectations and come through 2023 even more resilient. With the help and input of its members, MAPP continues to strive to provide meaningful insights to equip its members with the best intelligence available in the industry to grow and thrive in today’s dynamic global economy.

Further analysis is available by purchasing the 2023 State of the Plastics Industry Report through www.mappinc.com. The 2022 Machine Rate Report, with updated machine rates as of December 2022, also is available for purchase at www.mappinc.com. To become a member of MAPP, email the MAPP staff at info@mappinc.com.