By Teri Samples, partner and CPA, Wipfli

The Inflation Reduction Act (IRA) gave a boost to the manufacturing industry. Specifically, the new law rewards plastics processors for various investment initiatives to either incentivize or reward taxpayers who engage in a variety of clean energy practices. Many times, these investments make good business sense, with shorter than expected returns on those investments.

Many plastics processors and others within the plastics ecosystem including factories, workers, partners and building owners – may be eligible for incentives, deductions and credits.

Making Manufacturing Buildings Energy Efficient

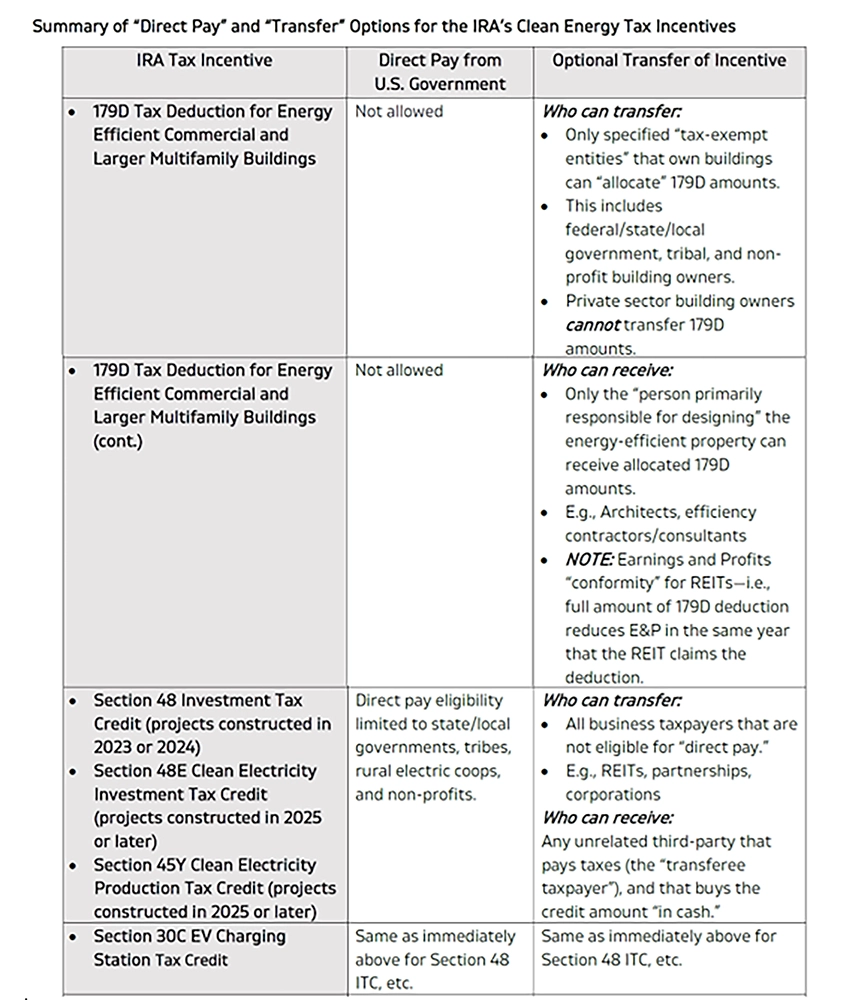

Section 179D: Building energy efficiency

Mike Devereux, a partner at Wipfli, has spoken several times at MAPP Plant tour events, talking about tax savings for energy-efficient improvements that manufacturers can make to their plants. Building energy efficiency, known as Section 179D, is a tax deduction whereby the owner of the building could receive a tax deduction of up to five dollars per sq. ft. for energy-efficient systems placed in service beginning Jan. 1, 2023. Previously, this was $1.80 (increased for inflation to $1.88).

If an owner of a manufacturing facility qualifies for this deduction through new construction or substantial renovations that meet the newly set energy standards, the owner may receive an accelerated deduction. To maximize the Section 179D deduction on commercial buildings, the energy efficiency must be 50% or higher, and the owner of the building also must meet the new prevailing wage and apprenticeship requirements. The deduction is on a sliding scale based on energy efficiency and prevailing wage requirements.

Section 179D: Retrofitting existing buildings

An alternative deduction around Section 179D relates to retrofits that renovate and rehab existing buildings. One of the biggest differences is that the baseline used to measure efficiency is not the same as for a newly constructed building. In the case of a retrofit site, energy use intensity reduction is measured against the pre-retrofit baseline. The more energy usage saved from a retrofit, the greater the deduction.

To be eligible for this alternative deduction, the building must be five years or older to qualify, and the deduction only can be claimed by the taxpayer after the energy-efficient equipment/systems are in service for one year. The anticipated project results must be certified by a third-party architect or engineer to show the efficiency achieved. Therefore, the deduction is not claimed in the year the capital expenditure was incurred for the project but rather a year later after certification.

As with Section 179D on new construction, the deduction cannot exceed the capital expenditure outlay for the project. It is capped at that amount.

Section 48: Solar and geothermal

Plastics processors can claim a tax credit based upon investment in solar and geothermal energy. Both the solar and geothermal credits in Section 48 begin at the six percent base rate of the investment, increasing to a maximum of 30% for projects where the prevailing wage requirements are met.

The credit applies in the year you place the system in service. The depreciable basis of the qualifying property will be reduced by half of the credit amount for determining future depreciation. The energy property qualifies for an asset class life of five years. Therefore, under the current bonus regime in 2023, the taxpayer would be able to deduct 85% of the remaining basis after the reduction of the credit amount.

This credit qualifies for direct pay in certain situations.

Section 30C: EV stations

The Section 30C tax credit for electric vehicle charging stations has been extended through 2032. The same base rate of six percent with a maximum of 30% as previously discussed also applies here. The credit is capped at $100,000 for each charging station or refueling pump installed at a property.

Third-party transferability applies, meaning processors can sell unused tax credits.

Producing Green Materials

Section 45X: Advanced manufacturing production credit

Manufacturers that produce components and materials required for solar, battery and wind devices could be eligible for an advanced manufacturing production credit under Section 45X. This particular credit could have significant benefits for domestic manufacturers and is based on efficiency of the product or piece vs. price or size. The IRS is expected to issue guidance on this credit soon, explaining how plastics processors can claim this credit for component parts it’s making in 2023 and thereafter.

Section 48C: Advanced energy credit

The IRA also extended and enhanced the advanced energy credit (Section 48C), with the goal of expanding US manufacturing capacity and quality jobs for clean energy technologies (including production and recycling), reducing greenhouse emissions and securing domestic supply chains for critical materials that serve as inputs for clean energy technology production.

Now, Section 48C includes $10 million in new 30% investment tax credits. The base credit is six percent, increased to 30% of project capital investment qualifying as energy property. The taxpayer must satisfy the prevailing wage and apprenticeship requirements in order to achieve the higher 30% credit.

Eligible property is tangible personal property or other tangible property (not including a building or its structural components), and it must be an integral part of the qualifying advanced energy project for which depreciation is allowed. There are a variety of ways to achieve this, including:

- A project that re-equips, expands or establishes a manufacturing facility for production or recycling of property used to produce energy from certain energy areas or designed to capture, remove or use carbon oxide emissions.

- A project to produce equipment designed to refine or blend any fuel, chemical or product that is renewable or low carbon/low emission.

The credit also covers infrastructure related to grid modernization, carbon capture, EV production and energy storage.

Manufacturers that operate in or adjacent to an energy community have been allocated 40% of the allocated credit dollars set aside for new clean technology manufacturing facilities. There is an application process, and the project must receive certification from the IRS in order to obtain the investment credit allocation, so it’s important to begin the process and planning early.

Limiting Emissions

Section 45Q: Carbon capture

A technology known as carbon capture use and sequestration (CCUS) is critical in achieving net-zero emissions, as it is a proven method of reducing greenhouse gas emissions from energy-intensive manufacturing facilities as well as industrial and power plants. CCUS involves capturing carbon and either storing it or using it to produce new products.

Neither this technology nor the Section 45Q tax credit relating to it is new; however, the costs involved and the fact that incentives only applied to major operators have previously limited CCUS’s application. Now, lowered requirements in the IRA have improved incentives and enhanced the viability of CCUS.

Section 45Q is subject to a tiered credit system with a lower base rate and a higher rate if the prevailing wage and apprenticeship requirements are met. The top potential rate is now $85 per metric ton of qualified carbon oxides captured and sequestered.

This applies when capture equipment is directly installed at the manufacturing or industrial facility. For direct air capture projects, the top potential rate now is $180 per metric ton. The annual carbon capture thresholds have been lowered from 18.750 to 12.500 metric tons per year and in some cases to 1,000.

Perhaps most importantly, companies now can elect a limited five-year direct pay option for Section 45Q tax credits. This allows companies that may not otherwise be able to use these credits to monetize them. They also have the option to sell these credits one time for cash per facility per year.

Energy Communities

The US Department of the Treasury and the US Internal Revenue Service have released new guidance regarding the Inflation Reduction Act for so-called “energy communities.” These energy communities incentivize by way of additional tax credit to develop energy projects primarily in places that historically have depended on fossil fuels in their local economies.

There is an additional bonus credit of up to 10% for Section 48 technologies that are installed in “energy communities.”

Three types of energy communities qualify for the tax credit. The categories include:

brownfields, which typically are small plots of polluted land; areas that meet certain percentage requirements for rates of employment in fossil fuel industries or tax revenue from fossil fuel activities;

and communities in which a coal mine closed after 1999 or a coal-fired power generating unit closed after 2009.

In conjunction with the IRS’s release of the guidance, the White House announced a mapping tool (https://energycommunities.gov/energy-community-tax-credit-bonus/) to help identify two types of potential energy communities: former coal communities and qualifying communities with employment or tax revenue related to fossil fuels. The map does not show brownfield sites.

Start Planning Energy Tax Credits and Deductions

By focusing on manufacturing and technological innovation, the changes made by the IRA are designed to stimulate and encourage investments related to making the manufacturing process cleaner and more efficient while decreasing its carbon footprint.

The credits or deductions applicable are significant, so it’s important to talk to a tax advisor specializing in these incentives now to discuss eligibility, what to pursue and how to get started.

Over the past 35 years, Teri Samples, partner and CPA with Wipfli has built a solid reputation as a trusted advisor and consultant specializing in real estate and construction, tax services, 179D/45L and cost segregation studies. Samples has extensive knowledge of federal agency energy incentives including tax deductions and credits. She is a member of the American Institute of Certified Public Accountants, Missouri Society of Certified Public Accountants, Home Builders Association, among many other memberships. Samples has a Bachelor of Science in Accounting from Southern Illinois University at Carbondale. Wipfli ranks among the top 20 accounting and business consulting firms in the nation and provides a range of services including energy, technology consulting, organizational performance, litigation services, compliance, tax consulting, cybersecurity and much more.

More information: www.wipfli.com.