By Andrew Carlsgaard, benchmarking and analytics director, MAPP

Healthcare and benefits strategy remains one of the most consequential business decisions US manufacturers make each year. In 2026, employers continue to face rising health benefit costs, tighter operating budgets and greater pressure to use benefits as both a retention tool and a financial management lever.

For many manufacturers, healthcare is no longer just a line item in the benefits budget; it is a core business plan issue that affects recruiting, retention and long-term competitiveness. That reality especially is true for smaller and mid-sized employers, which often have fewer options for absorbing annual cost increases without making trade-offs elsewhere in the business. Coupled with additional environmental pressures of inflation, tariffs and global supply chain disruptions, decisions on benefits could prove vital to maintaining profitability.

The results of the 2026 MAPP Health and Benefits Survey show that healthcare remains central to the value proposition for manufacturing employers. Nearly all respondents offer healthcare and conduct annual open enrollment, and most (96%) continue to rely on brokers to support the renewal process in 2026. The data also shows continued movement away from fully-insured coverage (57% of respondents in 2026, down from 61% in 2025) and toward more self-insured (29%) and level-funded arrangements (14%), reflecting a growing preference for greater control over cost and plan design.

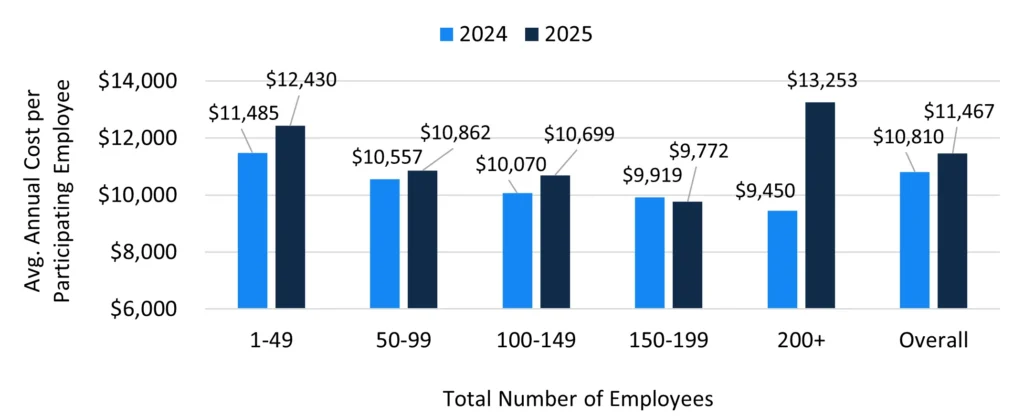

The 2026 Health and Benefits Report findings (Figure 1) also show that fully-insured healthcare costs remain elevated across employer sizes, with the overall average cost per employee increasing 6.1% from $10,810 in 2024 to $11,467 this past year. For context, the average was $9,289 in 2022, and 2025’s average would represent a $2,100-plus (23.4%) increase in cost per employee in just four years.

The broader market reinforces the same direction. A survey by the global professional services firm Mercer 1 expects employer health benefit costs to rise sharply again (6.7%) in 2026. The main drivers include higher medical utilization, specialty drug spending and continued pressure from pharmacy and hospital costs. Additionally, the outlook in Brown & Brown’s Employer Health and Benefits Strategy Survey 2 indicates continued pressure unless employers make active changes to their plans. It cites trends in inflation and the labor market, the prevalence of GLP-1 and biosimilars, and the increasing volume of large claimants as reasons requiring proactive planning by employers.

The Kaiser Family Foundation (KFF) 3 likewise notes that 2026 healthcare costs are being shaped by persistent premium pressure and other structural cost drivers. Among these pressures, the report mentions upward premium pressure, regulatory changes regarding cost transparency and broader affordability concerns stemming from healthcare provider consolidation. These external forecasts indicate that manufacturers are operating in a market where cost pressures are not easing, and employers must stay alert to avoid being caught flat-footed at renewal.

Taken together, those external analyses align closely with the data from the 2026 Health and Benefits Report. Manufacturers are not simply reacting to a difficult market after the fact; they are increasingly adjusting their designs, funding and employee contribution levels in advance of renewal. That shift is visible in the survey’s growing use of high-deductible plans, increased HSA contributions and other cost-containment strategies. In that environment, proactive benefits management is becoming a competitive requirement rather than a discretionary best practice.

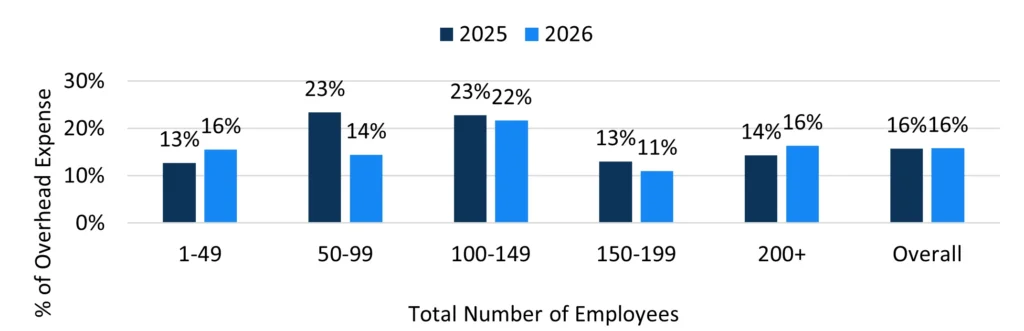

Company size continues to shape how manufacturers respond to these pressures. Smaller employers remain more sensitive to healthcare costs as a percentage of overhead, while larger employers are more likely to be self-insured and better positioned to use funding flexibility as a cost-management tool. As established in previous reports, the US Bureau of Labor Statistics 4 notes that the median age of manufacturing workers exceeds that of many other sectors, and an older workforce can place additional cost pressure on employer-sponsored insurance due to increased healthcare utilization, particularly in small- to mid-sized organizations (150 or fewer employees). The survey data (Figure 2) illustrates that healthcare remains a meaningful share of overhead, particularly for smaller employers. In practical terms, that means the same premium increase can have very different business impacts depending on the organization’s size and funding structure.

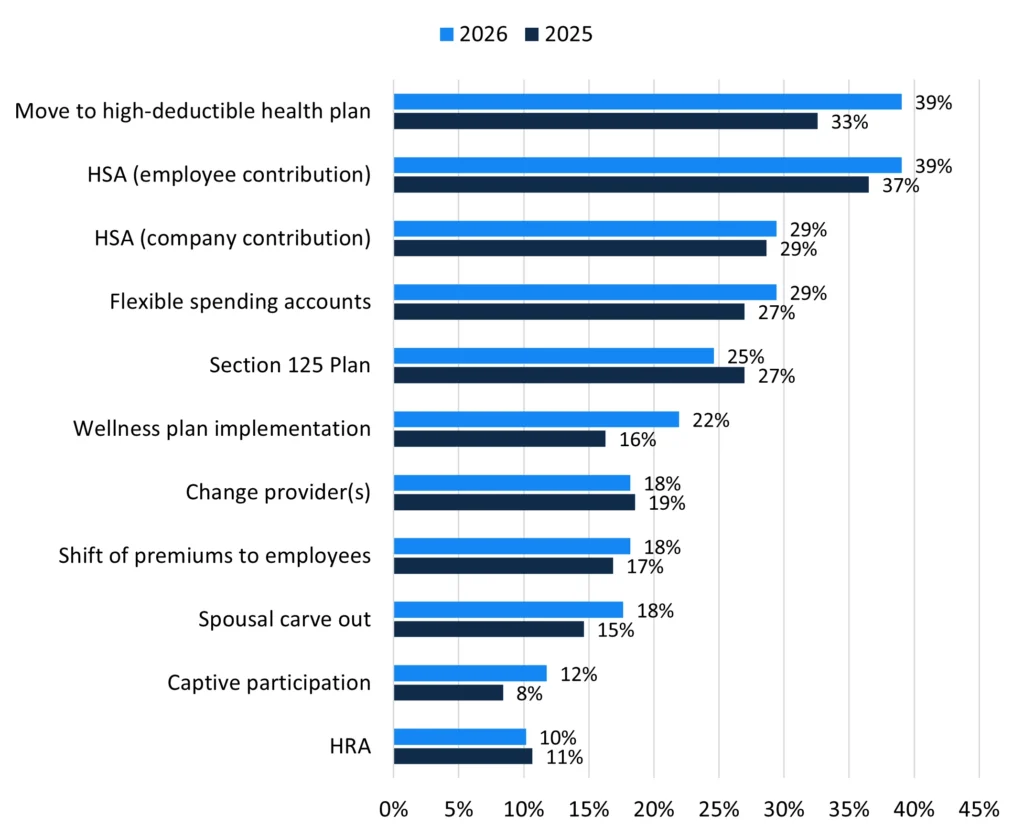

As a result, manufacturers also are becoming more deliberate in how they control costs. The 2026 report (Figure 3) shows that the most common strategies in 2026 include moving to high-deductible health plans, increasing employee HSA contributions, expanding wellness programs, changing providers and shifting more premium responsibility to employees. This points to a broader shift in employer behavior. Instead of relying on a single response at renewal, many employers now are using a layered approach that combines plan design, funding strategy and changes to employee contributions. That approach suggests a more mature and more disciplined benefits environment than in prior years. Notably, most of these tactics are available to self-insured or level-funded plan structures, whereas changing providers is the primary mechanism of cost control for fully-insured plans.

Overall, the 2026 survey describes a domestic manufacturing benefits landscape that remains under pressure, yet leaders are becoming more strategic. Manufacturing employers are paying closer attention to plan value rather than just plan price. As healthcare costs continue to rise, manufacturers increasingly need to help employees understand the tradeoffs among lower premiums, higher deductibles and out-of-pocket exposure. At the same time, employers still need to maintain benefits that support retention and hiring in a competitive labor market. This creates a balancing act that is becoming increasingly difficult, especially for small- and mid-sized employers that lack deep internal benefits expertise or strong advisory support beyond the broker.

Employers are working to preserve their competitiveness in the talent market while making more deliberate choices about funding, plan design and employee contribution strategies. The strongest organizations will be those that combine disciplined planning, better use of data and a willingness to revisit long-standing benefit assumptions before renewal pressure forces a decision. In this environment, proactive benefits management is no longer optional – it is a competitive advantage. n

Further analysis is available by purchasing the 2026 Health and Benefits Report through www.mappinc.com (the report is available free of charge to survey participants). If you are interested in becoming a member of MAPP, email info@mappinc.com.

References

- Mercer: Employer Health and Benefits Strategy Survey, https://www.mercer.com/en-us/about/newsroom/employers-and-workers-face-affordability-crunch-as-health-insurnace-cost-is-expected-to-exceed-18500-per-employee-in-2026/

- Brown & Brown: 2026 Healthcare Cost Outlook, https://www.bbrown.com/us/insight/2026-healthcare-cost-outlook/

- KFF: Eight Trends Shaping 2026 Health Care Costs, https://www.kff.org/health-costs/eight-trends-shaping-2026-health-care-costs/

- US Bureau of Labor Statistics: Labor Force Statistics from the Current Population Survey, https://www.bls.gov/cps/cpsaat18b.htm