By Andrew Carlsgaard, benchmarking and analytics director, MAPP

At the beginning of 2025, the United States plastics manufacturing industry is signaling recovery and growth. After several years of new economic challenges since the onset of the pandemic, including inflationary pressures and supply chain disruptions, optimism is on the horizon as the US manufacturing industry overall is projected (1) to experience a 4.2% increase in revenues and a 5.2% rise in capital expenditures. These positive trends are further supported by the Federal Reserve’s recent decision to lower interest rates by 0.75 basis points (2), which is expected to sustain manufacturing activity levels and encourage investment. Additionally, potential tariffs on Chinese and other foreign-made products are poised to benefit US manufacturers across all segments as many US-based customers may look to reshore their suppliers.

To track current plastics industry trends and assess momentum for 2025, MAPP surveyed 179 plastics manufacturing leaders from companies based in 34 different states on the status of relevant industry indicators, ranging from quoting to resin supply to operator wages. The results of these benchmarks for 2024 performance (both for the entire year and fourth quarter specifically) indicate increased optimism about 2025’s performance, despite improvements over the past year in some business metrics relative to a significant downturn in performance in 2022.

MAPP’s 25th annual State of the Plastics Industry Report aims to explore the business status over the US plastics industry’s 2024 fourth quarter and how its momentum can be analyzed to forecast growth and success going into 2025. Thus, the focus on revenue growth and margin in the upcoming 2025 fiscal year could be strongly influenced by 2024 sales performance, particularly with substandard momentum when considering sales growth over the fourth quarter.

2025’s State of the Plastics Industry Report showed another negative sales performance in the fourth quarter of 2024, with only 26% of respondents showing an increase during the quarter, down from 36% in the fourth quarter of 2023. This, in part, led to 45% of respondents reporting a year-over-year sales decrease for 2024 overall. Additionally, 36% of processors indicated sales declined over the same period at the end of 2024, tied with the fourth quarter of 2023 for the third-most significant number of respondents reporting declines in sales performance in the 21-year history of publishing this statistic in the State of the Plastics Industry Report.

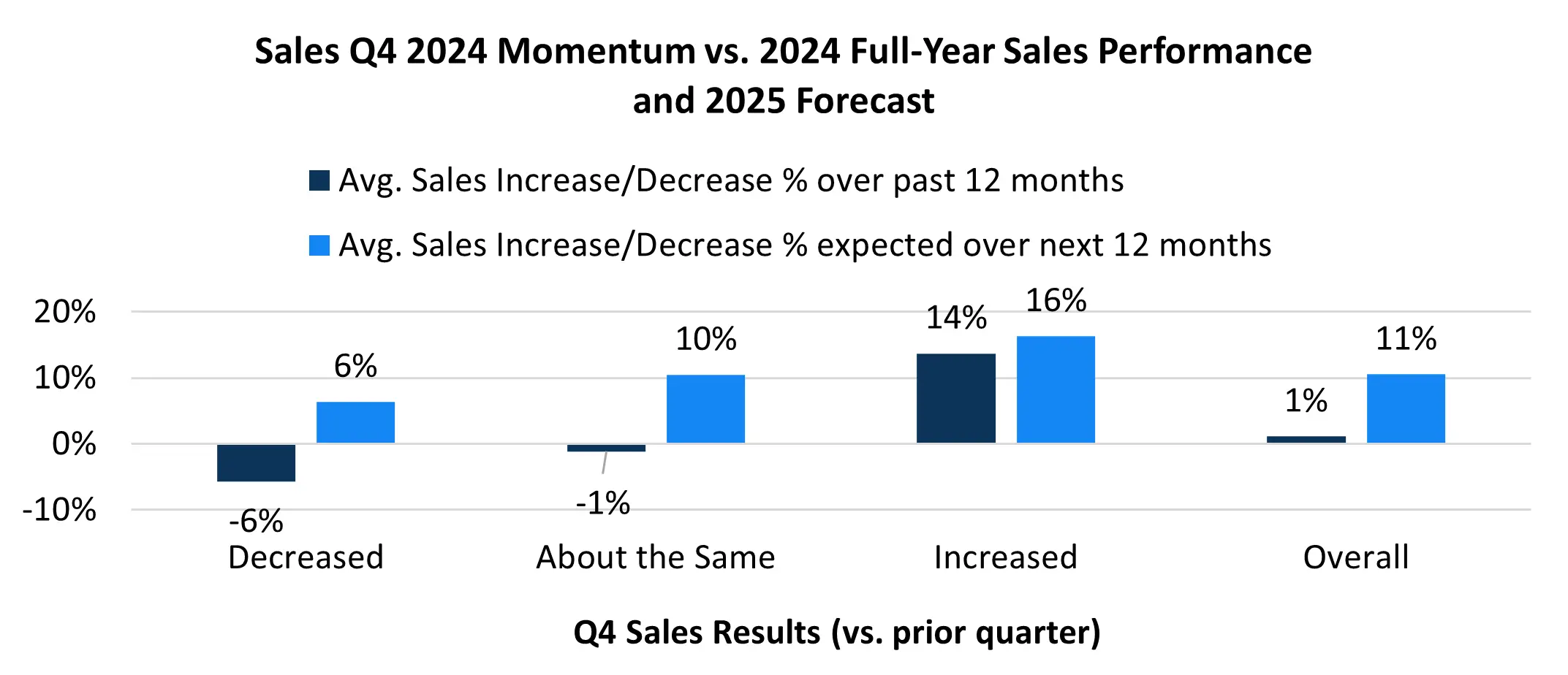

Fourth-quarter sales can propel or diminish the industry’s momentum going into a new year. Examining the five-year average of processors indicating increasing sales performance transitioning from third to fourth quarters provides reason for concern for at least the beginning of 2025. On average, over the last five years (2019-2023), 48%, or nearly half of the processors surveyed, have reported quarterly sales gains during the fourth quarter; however, only 26% reported increases in the fourth quarter of 2024 (Chart 1). Additionally, those reporting sales decreased in the fourth quarter from the third quarter also reported an average revenue decrease of 6% for the full year and forecast only 6% growth over the next year (2025), compared to increases of 14% and 16%, respectively, for those reporting increases in the fourth quarter (Chart 2).

Year-over-year sales increases continue to be attributed more often to new customers (33% in 2024). This trend has continued over the past two years, potentially signaling a necessary expansion of the industry’s client base over the past three years as the share of new sales coming from existing business has declined precipitously from two-thirds (67%) in 2020 to 43% at the end of 2024. However, despite revenue only increasing on average by 1% in 2024 overall, 77% of respondents anticipate sales increasing over the next 2025 calendar period.

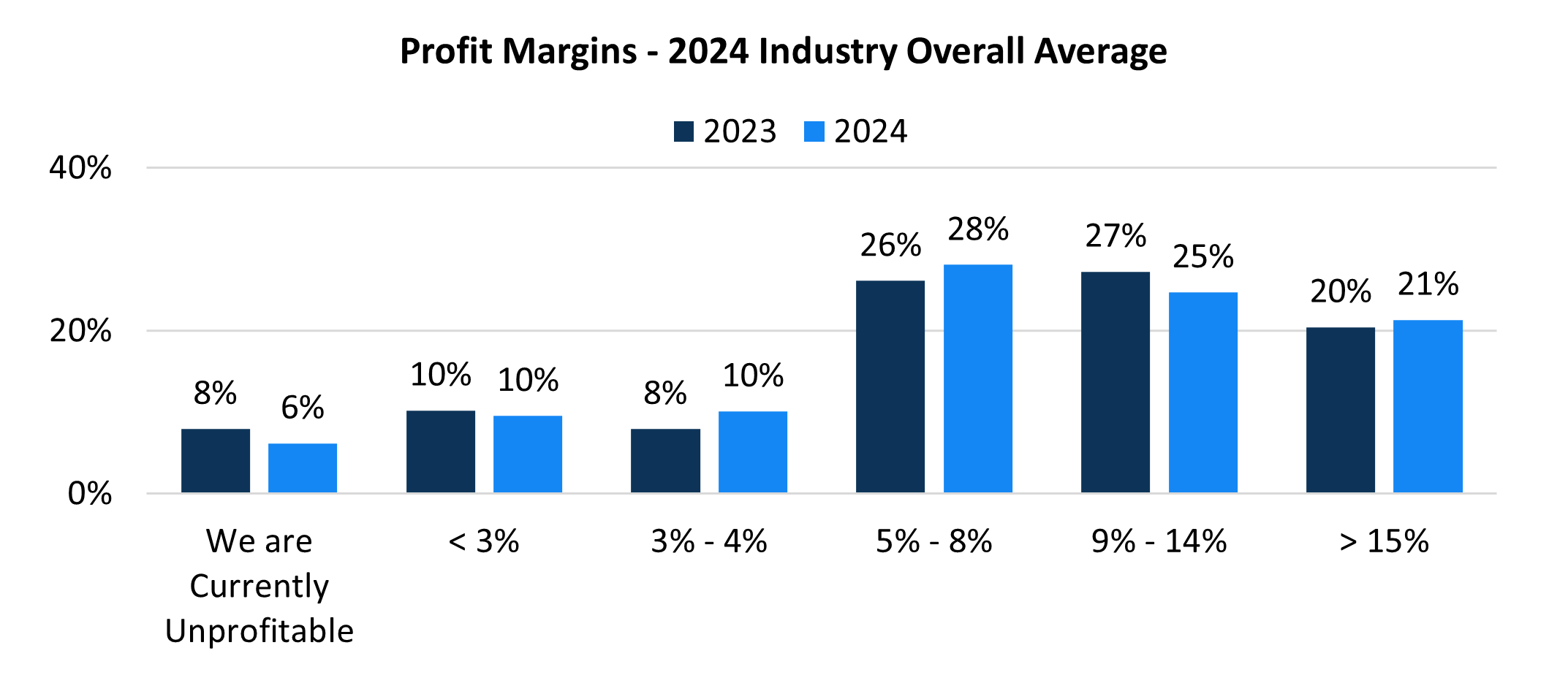

These slower sales increases at the end of 2024 also contributed to lower overall profits, as only around a fifth (20%) of the surveyed processors indicated that their profit (net income) had increased since the end of the third quarter of 2024 – down from 33% for the same time in 2023. When examining margins for the full year of 2024, nearly three-quarters of the respondents (74%) still realized profit margins of 5% or more, while 6% were unprofitable (Chart 3).

Of the reasons cited by respondents as their top three challenges interfering with profit margins, the most common were declining sales, rising inflation and increasing employee wages. This was the same top three as of a year ago, though declining sales now are the most top-of-mind as almost half of respondents (49%) listed it as the top challenge, while 15% put inflation as the highest concern. In addition, supply chain pressures and geopolitical tensions persist as ongoing challenges, with some downstream effects of tariffs and potentially increased transportation costs likely to increase production expenses and strain margins.

Despite these hurdles, there is a strong emphasis on innovation and sustainable practices within the plastics manufacturing industry. Businesses are investing in new technologies aimed at improving efficiency and reducing environmental impact. Also, the industry continues to grapple with a shortage of skilled labor, so companies actively are investing in training programs and automation to address this issue. This is evident due to plastics industry executives’ continued willingness to invest in the future of their businesses, as planned capital expenditures will increase in 2025 for over two out of five participants (44%). The top categories for capital spending dollars over the next year were primary machines and automation, which respondents consistently cited as critical pieces of their strategies to expand their business capabilities, upgrade their overall capacity and improve efficiency.

Market growth is anticipated in 2025 for the US plastics manufacturing industry – driven by strategic investments and favorable economic conditions for US-based processors. As a result, there is cautious optimism among industry leaders about the future of the sector, with a focus on innovation, sustainability and overcoming labor, inflation and supply chain challenges. Although a slow start is to be expected for the industry due to lagging metrics in the fourth quarter, improved processor sentiment, along with increased focus on investments and optimistic sales projections, paint a picture of a more robust 2025, with a stronger outlook over the next several years on the horizon.

Further analysis is available by purchasing the 2025 State of the Plastics Industry Report through www.mappinc.com.

References

1. Manufacturing Today: US Manufacturing Growth in 2025

2. PlasticsToday: The Known Unknowns Confronting the Plastics Industry in 2025