By Andrew Carlsgaard, benchmarking and analytics director, MAPP

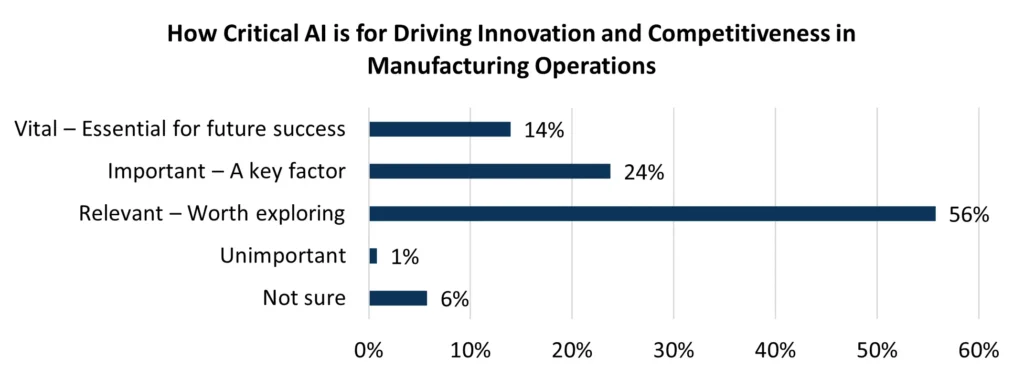

The results of the 2025 Artificial Intelligence Adoption Survey provide a precise and nuanced portrait of how US manufacturing leaders are deploying artificial intelligence (AI), particularly among members of the Manufacturers Association for Plastics Processors (MAPP) and the Association for Rubber Products Manufacturers (ARPM). AI is increasingly recognized as a crucial driver of competitiveness and innovation within the plastics and rubber product manufacturing sectors, with more than three-quarters of surveyed leaders labeling it as either relevant, important or vital to their future. (Chart 1) The survey reveals a high level of anticipation for the impact of AI, with a combined majority expecting it to make a significant operational difference within the next three years, and nearly one-third believing such impacts will materialize in as little as 12 months. Nevertheless, adoption is marked by reasonable caution by most respondents – while a small group already reports tangible, organization-wide results, most manufacturers surveyed remain in exploratory or pilot phases.

The results of the survey of 125 processors closely track with Deloitte’s 1 2025 Smart Manufacturing Survey, which found that a vast majority (92%) of surveyed US manufacturing executives believe smart manufacturing – including AI – will be the primary driver for competitiveness in the next three years, with a similarly large majority expecting a transformative impact on products, agility and talent attraction. Both datasets emphasize that operational and financial gains, such as improved production output, agility and employee productivity, are among the primary motivating factors for AI investment.

When comparing adoption rates, the plastics sector lags somewhat in terms of enterprise-wide deployments: while Deloitte reports that about 29% of respondents are using AI or machine learning at facility or network level, and 23% are piloting AI solutions, the MAPP survey data indicates only 6% of respondents currently seeing a direct business impact from AI, with most (88%) still in early pilot or knowledge-building phases. This echoes observations from the American Supply Association (ASA) 2, which reports that despite 93% of US manufacturers having adopted or experimented with AI in some way, meaningful and transformative adoption is just gathering momentum. Processors’ focus mirrors national trends, with administrative, finance, IT and production tasks among the key areas for AI experimentation – an alignment seen in both Deloitte and ASA findings.

Readiness to adopt and scale AI also is a standout challenge. Nationally, both Deloitte’s and Kyndryl’s 3 research highlights a significant skills gap in manufacturing, with nearly half of executives reporting moderate to severe difficulties in filling roles in operations, planning, scheduling and technology management. The survey found that 30% of processors rate their workforce as only “somewhat prepared,” 65% as “not prepared,” – a result almost mirroring Kyndryl’s report that just 35% of manufacturers consider their teams ready, and McKinsey’s survey showing manufacturing’s talent and readiness for AI trailing other sectors.

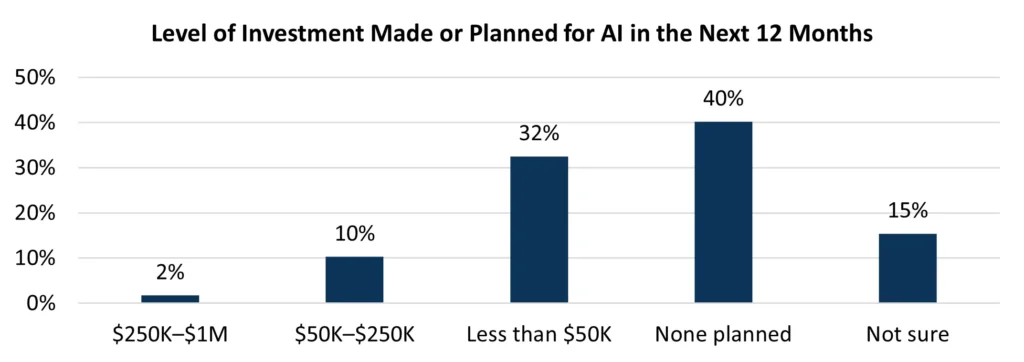

Regarding future investment levels in this new technology, processors remain cautious, as over half of respondents (55%) report having no imminent investment plans or are unsure whether there will be any over the next year. (Chart 2) In contrast, Deloitte documents that a majority (78%) of manufacturers surveyed nationwide are allocating more than 20% of their overall improvement budget to ‘smart’ manufacturing technologies, with a focus on skills training and cybersecurity.

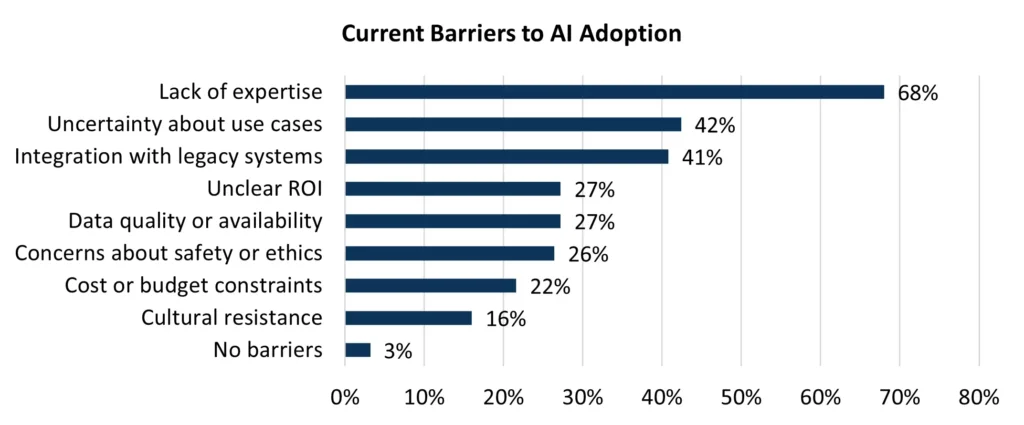

In terms of barriers, the most substantial hurdles – lack of expertise (reported by over two-thirds of respondents), unclear value for investment and integration with legacy systems – are closely aligned in both the MAPP survey and the wider manufacturing AI research from Deloitte, ASA and Kyndryl. (Chart 3) While productivity improvements and compelling operational gains are reported, progress toward advanced, cross-organization integration remains incremental, underscoring the sector’s need for ongoing support, talent upskilling and strategic direction.

In summary, the plastics manufacturing sector’s AI journey is consistent with, but somewhat more cautious than, the larger US manufacturing narrative. Most organizations are piloting AI in targeted functions, recognizing its strategic value, but struggle with readiness and skills gaps that align with national benchmarks. The sector joins the broader manufacturing industry in calling for accelerated knowledge sharing and practical guidance from associations, preparing the groundwork for more significant transformation in the years ahead.

For more information on the AI Benchmarking Report, visit www.mappinc.com/resources/benchmarking. To view the 2025 Best Practices Book, which features innovations in artificial intelligence, visit www.mappinc.com/resources/bestpracticesawards/best-practices-book/.

References

- Deloitte: 2025 Smart Manufacturing and Operations Survey

- ASA: AI Revolutionizes Manufacturing

- Manufacturing Dive: Kyndryl AI Manufacturing Survey